For the sectors not covered by EU emissions trading (especially heat and transport), the remaining EU climate target is distributed among the individual EU member states. To this end, the Federal Republic of Germany introduced its own national emissions trading system (nEHS) in 2021. By putting a price on potential CO2 emissions from fuels, the aim is to create an incentive to become more climate-friendly and achieve the EU's climate target. The distributors of fuels are obliged to purchase a corresponding quantity of certificates for the potential quantities of CO2 emissions from the fuels they put into circulation. The responsible authority is the German Emissions Trading Authority (DEHSt) at the Federal Environment Agency (UBA).

In order to determine the quantity of fuel emissions placed on the market, distributors are required to prepare an annual emissions report and submit it to DEHSt.

The CO2 certificates are sold via the EEX and entered in a national emissions trading registry (nEHS registry).

In contrast to European emissions trading, it is not the plant operators but the distributors of fuels who are required to participate. This includes in particular gasoline, diesel, heating oil, natural gas and, from 2023 on, coal. This means that gas suppliers and companies in the petroleum industry that pay energy tax are particularly affected. In principle, the person liable to pay tax under the Energy Tax Act (EnergieStG) is defined as the distributor.

Coal is subject to the special rule that it will also be covered by the BEHG from 2023 if it is used free of energy tax. The goods covered by the BEHG are listed in Annex 1 of the BEHG. From 2024 on, operators of plants requiring a permit pursuant to 8.1.1 and 8.1.2 of Annex 1 of the Ordinance on Installations Requiring a Permit, i.e. waste incineration plants, will also be subject to the nEHS.

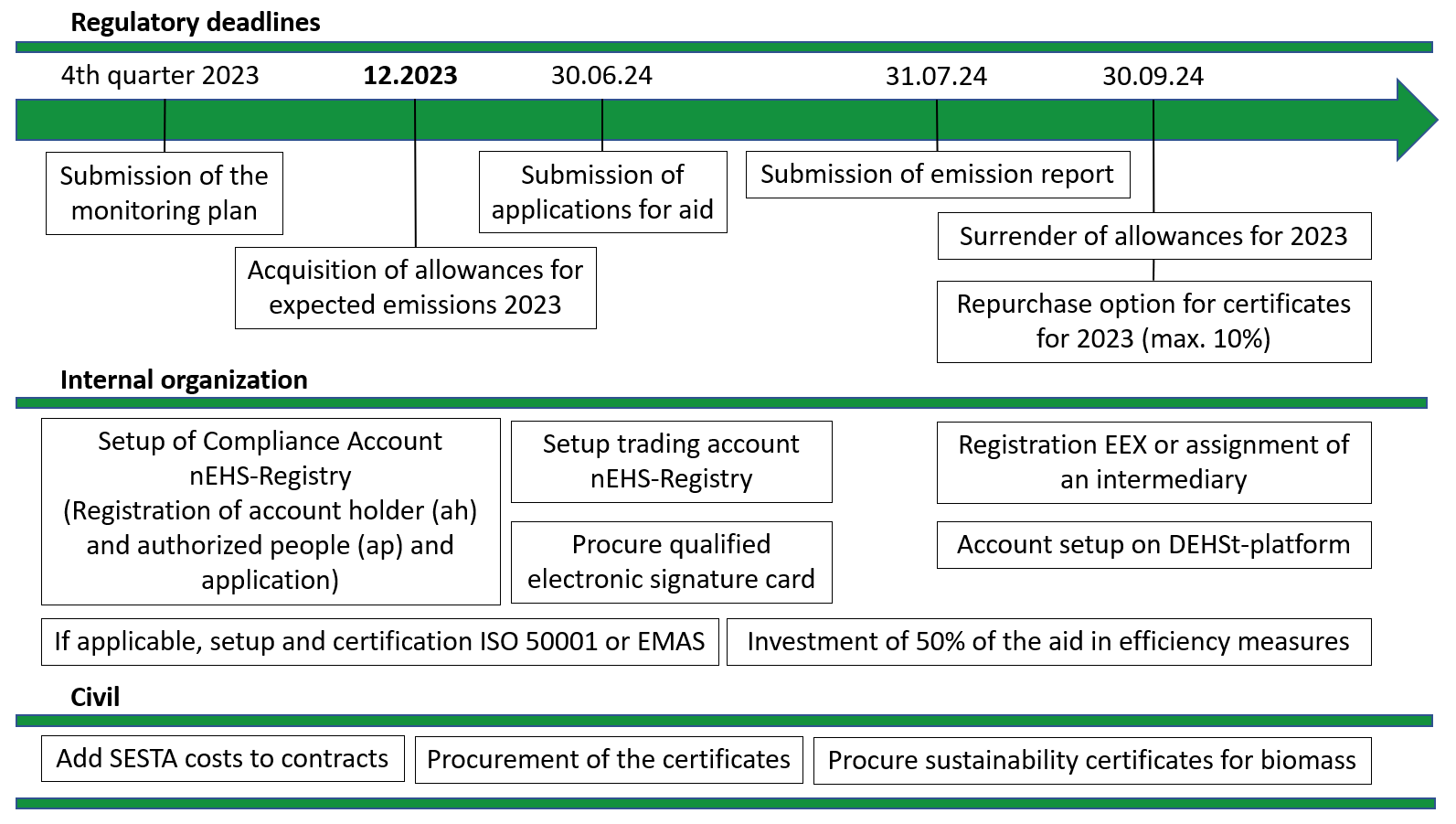

A monitoring plan must be submitted to DEHSt for the reporting year 2024 and the following years and must be approved

From the 2023 reporting year onwards, annual emissions reports must be submitted via the DEHSt platform by 31 July of the following year

Waste incineration plants do not have to submit their emissions reports until 2024

Purchase of emission certificates on the EEX

Surrender of emission allowances via the nEHS registry

Similar to European emissions trading, the Renewable Energy Directive (REDII) also applies to biomass in national emissions trading.

The emissions from biomass can thus be deducted if proof of their sustainability is available. The proof is provided by the Nabisy system of the BLE.

For the year 2023, BEHG officers may make use of the transitional rule for the obligation to provide evidence of the biogenic share if one of the following situations applies:

The responsible person has not yet been able to carry out certification due to a lack of a certification system, or

The responsible person could not perform certification due to lack of capacity of the certification bodies.

The certification process must nevertheless be initiated without delay.

Currently, there is the problem that Nabisy does not yet issue certificates for solid and gaseous biomass. For 2023, DEHSt will therefore accept the following certificates:

If there is no certification of the responsible party or the upstream chain, a self-declaration and traceable mass balance is sufficient.

If a certification of the responsible party or the upstream chain already exists, the corresponding proof of a recognized system is accepted.

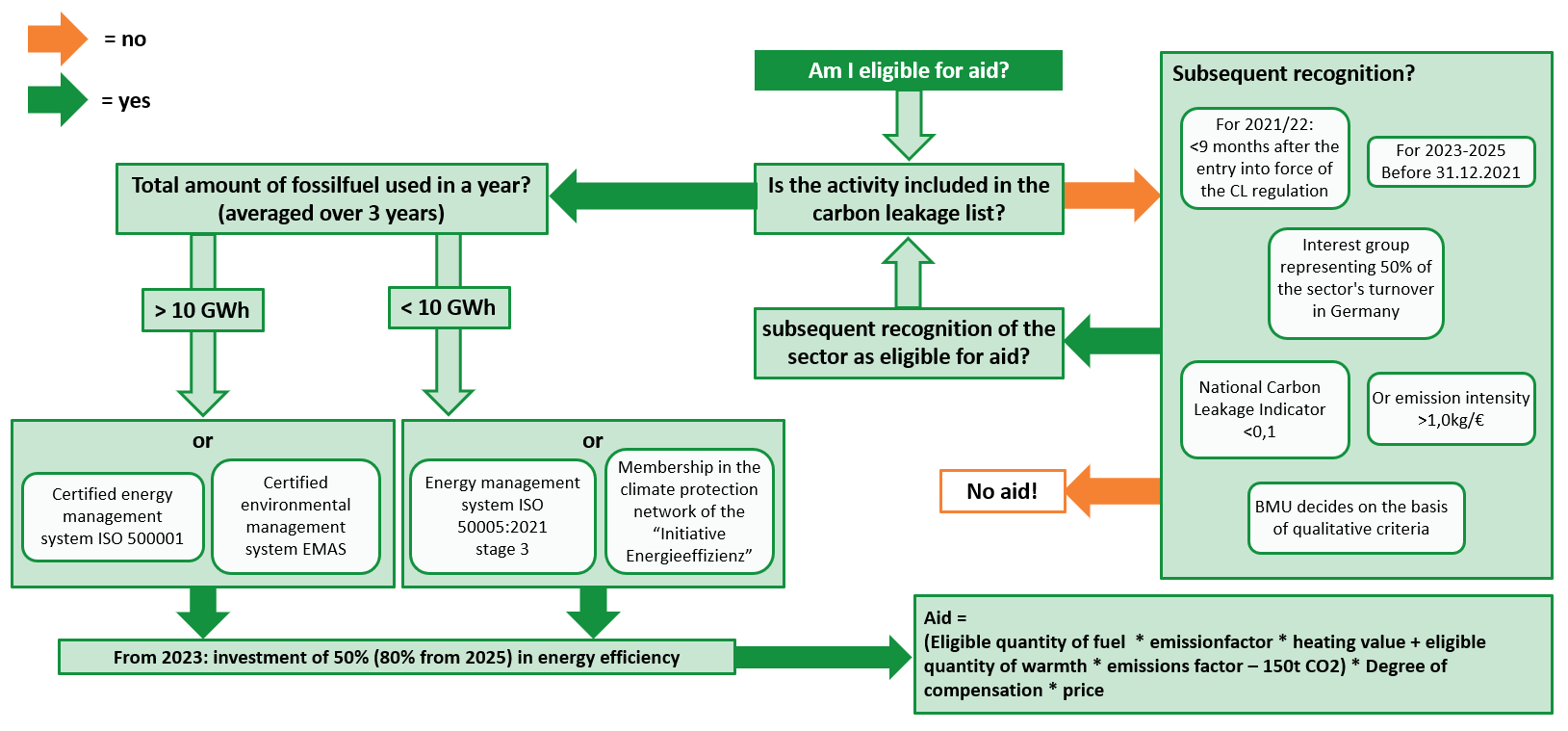

Am I eligible for aid under the Fuel Emissions Trading Act?

Thanks to the Carbon Leakage Regulation (BECV), companies will be able to receive subsidies from 2021 if they operate in a sector eligible for aid of the EU ETS. To do so, they must have a certified energy management system according to ISO 50001 or an environmental management system according to EMAS (note: ISO 14001 is not allowed so far) from 2023 and provide evidence of investments in decarbonization or energy efficiency. The level of investment must be more than 50% (80% from 2025) of the previous year's aid and can be spread over four years.

Permissible for small emitters of less than 10 GWh of fossil fuels is a non-certified energy management system according to DIN EN ISO 50005 or membership in an energy efficiency and climate protection network registered with the German Energy Agency.

For an average plant, the sector affiliation and the NACE code are first determined. The degree of compensation can be read from the table in the appendix. Depending on the fuel used, the emission factor results as one of the default values of the Emission Reporting Regulation 2022 (Annex 1 Section 4).

Aid = (fuel quantity * emission factor * calorific value -150t CO2 ) * degree of compensation * price

Thus, only the amount of fuel needs to be determined. For example, a plant burning 7,000 Nm3 of natural gas for the processing of aluminium (NACE code: 24.42) is expected to receive aid of €314,145. On the other hand, the production of electricity and heat for a district heating network does not receive aid, and the costs can be passed on to consumers.

According to Annex 1 of the SESTA, the following fuels are to be reported:

Coal

Fuel oil, liquid gas

Natural gas

Gasoline

Diesel

Vegetable oils

Anti-knock and lubricant

Hydrocarbons used as fuels or heating fuels

Methanol

Fuels are also goods used in the case of §2 par. 2a BEGH in the facilities mentioned therein.

Which steps are required for compliance?

Preparation of a monitoring plan (mp), valid as of 2024

Register account holder (ah) and account authorized people (ap) in the nEHS registry.

Submit an application to open an account in the nEHS registry

Submit documents for registration of ah and ap in the nEHS registry

Apply for admission to the EEX or use an intermediary

Review of the emission reports

Since 2023, the emission reports are subject to a verification obligation. Provided that a simplified OB is available and no deductions due to tax relief are claimed, verification is not necessary. Verification is not necessary for installations requiring a permit if the fuel emissions are determined mathematically using default values and the fuel quantities have already been verified as part of an audit of the register of guarantees of origin. A site visit is required for verification of emission reports unless a simplified monitoring plan is used.

GUTcert is also accredited as a verification body for the nEHS from 2023 on. We also help shape relevant issues in various working groups and committees. As an experienced testing organisation for environmental and energy management, we also certify within the framework of the state aid procedure – feel free to contact us.

We would also be happy to speak about the latest developments at your event or in your energy efficiency network.

What is the cost of verification?

We calculate the cost of verification individually, depending on the complexity of the company and the data procurement effort. Please do not hesitate to contact us.

Further information on the certification process can be found here.

The Emissions Reporting Regulation (EBeV 2030) and the BEHG (German Emissions Trading Act) Double Accounting Regulation (BEDV) (both German regulations) regulate the overlaps between the nEHS (National Emissions Trading System) and the existing EU ETS (Emissions Trading System) system. Based on the principle that each tonne of CO2 is only priced once, there are two options.

Option 1: According to Section 17 of the EBeV 2030 (the German law on the energy transition), the BEHG-responsible party (the party responsible for the energy transition) can deduct the fuel quantities that it supplies to a facility subject to the EU ETS (the European Union Emissions Trading System). This requires an identical declaration from both parties, the ‘Verwendungsabsichtserklärung’ (Intention to Use Declaration), stating that the fuel quantities of the BEHG-responsible party are intended for use in the EU ETS facility. The use is verified by the EU ETS installation's confirmation of use, which is generated from the EU ETS emissions report.

Option 2: If the above advance deduction is not possible and the fuel quantity is passed on to the EU ETS installation with the CO2 price, it can be reimbursed. To this end, the EU ETS installation must submit a compensation application based on the verified emissions report. This must be submitted by 31 July.

As part of the ‘Fit for 55’ package, it was decided to expand emissions trading and establish a system similar to the German national emissions trading system to cover the building and transport sectors. As in the BEHG, those responsible are the persons liable for tax.

EU ETS 2 will therefore apply from 2024. For the years 2024 to 2026, there will initially be a reporting obligation only, with no obligation to pay a levy. There will also be no verification obligation for 2024. For the reporting year 2025, there will be a verification obligation for the first time.

The deadline for submission is always 30 April of the year following the reporting year.

This means that there is initially a double reporting obligation due to the parallel systems.

SESTA Carbon Leakage Ordinance (BECV)

Fuel Emissions Trading Ordinance (BEHV)

SESTA Dual Accounting Ordinance (BEDV)

Emission Reporting Ordinance 2030 (EBeV 2030)

Please also note the tax regulations from the Energy Tax Act (EnergieStG) and the regulations on biomass from the Biomass Electricity Sustainability Ordinance (BioSt-NachV)

Independent, professional, timely verification of emissions and emissions reports

Verify the compliance of the monitoring and reporting methodology (monitoring plan) with the applicable regulations

Within the scope of the audit report, concrete recommendations and indications for the improvement of the emission data management system and the structures for quality assurance and control

Regular information on current developments and changes in emissions trading through our newsletter and various events of the GUTcert Academy

Transparency: You benefit for your future annual reports from a detailed audit report with tips for systematic improvement of your data quality and process descriptions.

Efficiency: Your time expenditure is minimised and timely verification is guaranteed if the contract is awarded in time –thanks to our broad-based environmental verifier and auditor pool: We are many, fast and effective.

Industry knowledge: Our subject matter experts know what you are talking about – they are familiar with your industry, have many years of experience in emissions trading, and are additionally qualified to certify to ISO 14001, ISO 9001, or ISO 50001, among others, if required.

Contact persons: You are always up to date with the latest developments, also in national emissions trading, and can rely on competent contact persons in all procedural matters at all times with our central energy team.

Global network: Your worldwide branches are in good hands with us – thanks to our global network within the AFNOR Group. We speak your language, no matter where.

Fortschritte bei der Überarbeitung der Scope-2-Guidance

Die GHG Protocol Initiative arbeitet derzeit an einer Aktualisierung ihrer Unternehmensstandards, da-runter die im Jahr 2015 veröffentlichte Scope-2-Guidance.

SBTi veröffentlicht Net-Zero-Entwurf für die Automobilbranche

Entwurf kommentieren und an Pilotprojekt teilnehmen: Der neue Entwurf für Automobilhersteller und Zulieferer kann bis 11. August 2025 öffentlich begutachtet werden.

18.11.2025: Der Emissionshandel-Betriebsbeauftragte der 4. Handelsperiode

Im diesjährigen Erfahrungsaustausch informieren wir als Prüfstelle über Neuerungen im Emissionshandel und sind gespannt auf die Erfahrungen der geladenen Expertinnen und Experten.

Kompensationsanträge 2024: Fristen und Hinweise zur Antragsstellung

Bis zum 31. Juli 2025 können Anträge auf ETS-Kompensation eingereicht werden – wichtige Infos zur Antragsstellung und für rückwirkend emissionshandelspflichtige Anlagen.