Corporate Carbon Footprint (CCF) - The GHG footprint of your organisation

What is a Corporate Carbon Footprint?

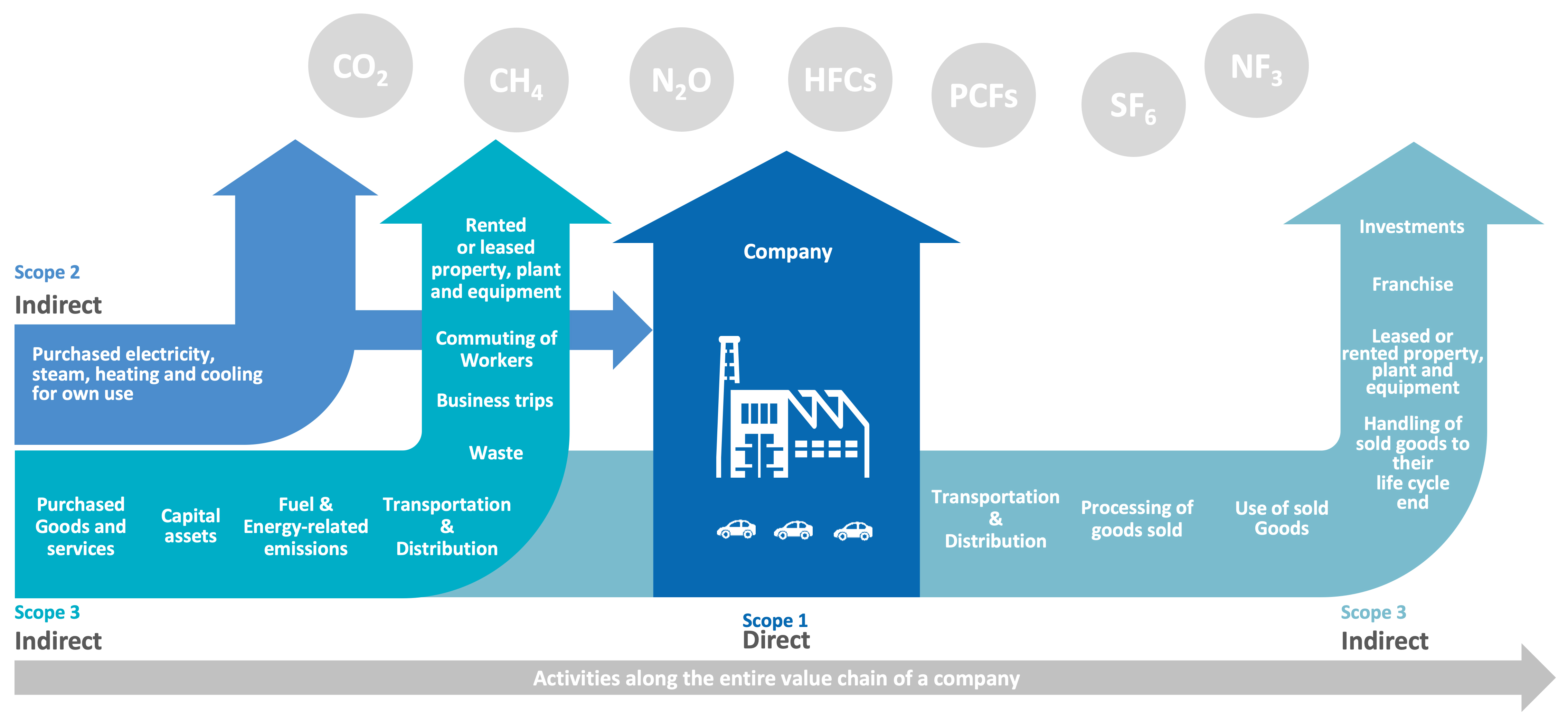

The Corporate Carbon Footprint (CCF) is the GHG footprint of organisations. It is made up of the direct and indirect greenhouse gas emissions of the entire organisation: in the company itself, at a location or at a part of the company.

Direct emitters include, for example, the company's own power plant or vehicle fleet, but also industrial processes such as cement or lime production.

Indirect emissions outside the company boundaries include, for example, travel by employees or from the customer area, but also transport and others.

The CCF comprises 3 scopes:

Scope 1: Emissions generated directly within the company, at a site or part of the company (e.g. from the use of the company's own power plant or vehicle fleet)

Scope 2: Indirect emissions resulting from a company's energy purchases (e.g. from the purchase of electricity and heat)

Scope 3: Indirect emissions along the value chain (e.g. business trips, production of supplier products, transport)

Source: Illustration from the guideline "FROM ENERGY MANAGEMENT TO CLIMATE MANAGEMENT (DENEFF)", based on GHG Protocol

Why calculate a corporate carbon footprint?

How much greenhouse gas (GHG) does your organisation or company produce? Are you meeting your own climate protection requirements?

The CCF forms the basis for developing a climate strategy. Specific reduction targets and measures can be derived from the information obtained on emission sources. The systematic approach enables reliable communication to the outside world and to stakeholders.

A CCF is also a basic requirement of the Corporate Sustainability Reporting Directive (CSRD), which is already mandatory for large parts of European companies or will soon become relevant.

What are the benefits of verifying the corporate carbon footprint?

A carbon footprint serves as a management tool for the implementation of GHG and cost reduction plans. In addition, a clear climate strategy for reducing global warming can be developed on the basis of the corporate carbon footprint.

External verification of the GHG balance safeguards reporting, improves your reputation, serves as proof of the credibility of your climate management and can be used as preparation for the requirements of the CSRD.

A detailed check of the completeness and methodology you use to determine the data gives you a reliable basis for identifying your actual GHG sources

The standards define principles and requirements for quantifying and reporting GHG emissions and sinks. This includes the development, reporting and verification of an organisation's GHG inventory.

If you want to account for your organisation's greenhouse gases, you basically have the choice between two established standards:

ISO 14064-1: Greenhouse gases - Part 1: Specification with guidance for quantifying and reporting greenhouse gas emissions and removals at the organisational level.

Can it be integrated into or combined with other standards?

Systems on the basis of which environmental and energy data is already recorded (e.g. ISO 14001 or ISO 50001, emissions trading or the GRI standard) help when creating a CCF. This means that the necessary structures for collecting climate-relevant data are often already in place. Take a look at our guide "From energy management to climate management" for more information

We are happy to combine our verification of your GHG balance sheet with existing management systems or legal reporting obligations. Our auditors have multiple qualifications and can often audit several standards at the same time. Feel free to ask us about this and utilise synergies.

Verification of CCF tools and methodologies

In addition to specific greenhouse gas balances, accounting tools and methodologies can also be checked and confirmed against the above standards.

Any software solution that centralises and automates the collection and categorisation of greenhouse gas-relevant information and the calculation and balancing of greenhouse gases for reference values is a carbon footprint tool. This includes, for example, Excel-based tools, browser-based applications or other customised software solutions.

Normative requirements, internal organisational ideals and increasing customer demands have led to a sharp rise in interest in greenhouse gas balancing - the market for carbon footprint tools is growing all the time.

An external, independent review not only sets you apart from your competitors, but also protects you against any risks and strengthens the resilience of your tool.

Especially with newly developed methodologies, it is helpful to ensure plausibility and functionality through an external review.

The calculation methods and (emission) data sources are compared with the requirements of the relevant standard by an independent body. In the case of organisation-independent tools, the check can be carried out entirely through remote sessions and a desk test. If identified deficiencies have been demonstrably rectified, you will receive a confirmation of conformity for your tool.

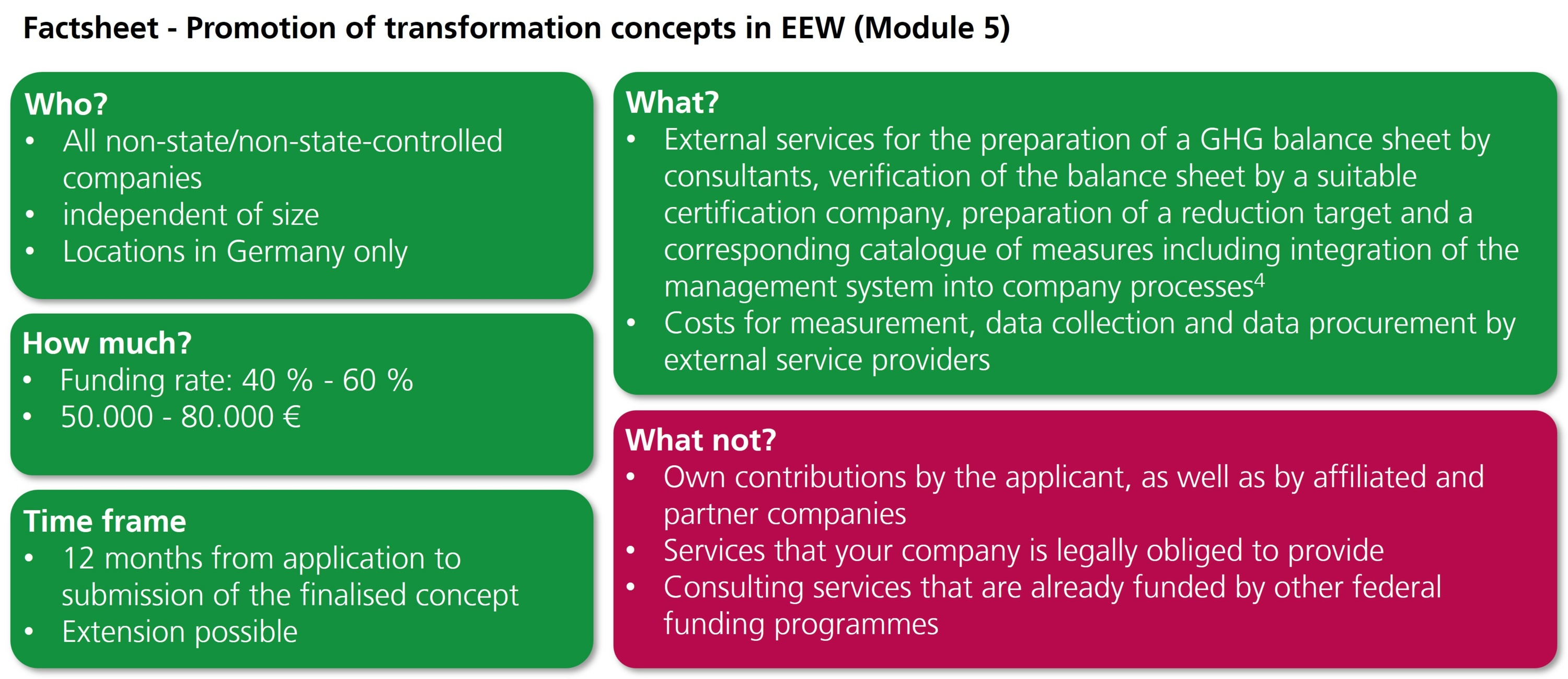

Verification of your greenhouse gas balance for state-funded transformation concepts

What are the transformation concepts promoted by the BMWK in the EEW?

In the funded transformation concepts, companies should present and analyse their methodology for recording current greenhouse gas emissions (actual state) as well as a long-term and concrete greenhouse gas target derived from this.

In order to achieve climate neutrality, the short-term and long-term decarbonisation strategies in the transformation concepts should also be backed up with concrete measures and savings concepts.

Important: Scope 1 and 2 are mandatory for the state funding of your transformation concept. Scope 3 accounting is optional. However, for systematic climate protection management and to safeguard your climate protection risks, a valid greenhouse gas balance sheet should always include the indirect emissions from Scope 3.

Fortschritte bei der Überarbeitung der Scope-2-Guidance

Die GHG Protocol Initiative arbeitet derzeit an einer Aktualisierung ihrer Unternehmensstandards, da-runter die im Jahr 2015 veröffentlichte Scope-2-Guidance.

SBTi veröffentlicht Net-Zero-Entwurf für die Automobilbranche

Entwurf kommentieren und an Pilotprojekt teilnehmen: Der neue Entwurf für Automobilhersteller und Zulieferer kann bis 11. August 2025 öffentlich begutachtet werden.

18.11.2025: Der Emissionshandel-Betriebsbeauftragte der 4. Handelsperiode

Im diesjährigen Erfahrungsaustausch informieren wir als Prüfstelle über Neuerungen im Emissionshandel und sind gespannt auf die Erfahrungen der geladenen Expertinnen und Experten.

Kompensationsanträge 2024: Fristen und Hinweise zur Antragsstellung

Bis zum 31. Juli 2025 können Anträge auf ETS-Kompensation eingereicht werden – wichtige Infos zur Antragsstellung und für rückwirkend emissionshandelspflichtige Anlagen.

Guide from energy management to climate management

Do you already have an energy management system in accordance with ISO 50001? Then you are not far away from climate management: Our guide shows you how to do this in a structured way - over 5 stages in 14 steps.